Strong margin, well positioned for growth

KEY HIGHLIGHTS

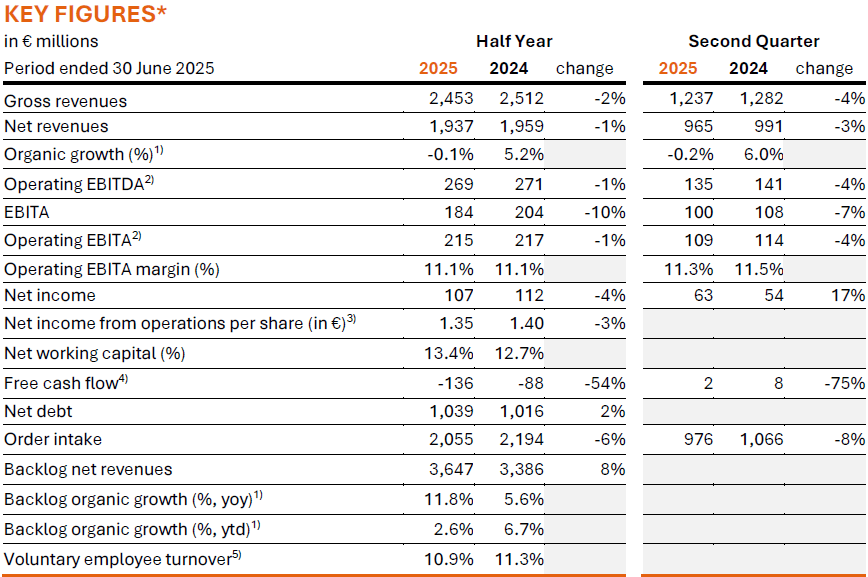

- Net revenues were €1,937 million: stable year-on-year on an organic basis

- Increased Key Client order intake further improving backlog quality (3% ytd organic growth)

- Strong operating EBITA margin of 11.3% in the quarter, with substantial strategic investments to accelerate future growth and further cost efficiencies

- Integration of recently acquired WSP Rail and KUA Data Centers unlocking new growth opportunities in Germany

- Well positioned for growth in the second half of 2025: large contracts ramping up, increased UK spending and improved market stability

Amsterdam, 31 July 2025 – Arcadis, the world’s leading company delivering data-driven sustainable design, engineering, and consultancy solutions for natural and built assets, reports €965 million net revenues for the second quarter, reflecting a stable performance on an organic basis year-on-year and continued operational improvements with an operating EBITA margin of 11.3% in the second quarter, while substantially investing in strategic initiatives to accelerate future growth and further cost efficiencies.

Alan Brookes, CEO Arcadis, said: “In the first half of 2025, Arcadis demonstrated good performance, with continued strong demand in North America and Europe offsetting more challenging conditions in UK and Australia. We increased our Key Client order intake and have further expanded our Global Excellence Centers to enhance project delivery and support our teams worldwide. Margin performance was strong while making substantial strategic investments to position us well for future growth and drive further cost efficiencies. Large contracts’ ramp up, a concluded UK Spending Review and the commencement of the water cycle AMP8 have positioned us well for growth in the second half of 2025. While some uncertainty around market dynamics remains, our healthy backlog and pipeline give us confidence in our future. With our clear strategy and the expertise of our people, we continue to be on track to achieve our 2024-2026 targets.”

* 2024 and 2025 half year results as presented in this press release are unaudited

1) Underlying growth excl. impact of FX, acquisitions, footprint reductions, winddowns or divestments.

2) EBIT(D)A excluding restructuring, integration, acquisition, and divestment costs.

3) Net income before non-recurring items (e.g. valuation changes of acquisition-related provisions, acquisition and divestment costs, amortization of intangible assets, expected credit loss on shareholder loans and corporate guarantees and one-off pension costs).

4) Free cash flow: cash flow from operations adjusted for capex and lease liabilities.

5) Voluntary employee turnover excludes the Middle East as these operations are being wound down.

REVIEW OF THE SECOND QUARTER 2025

NET REVENUES AND BACKLOG

Revenue growth was strong in the US, Canada, and the Netherlands, supported by high demand for Energy Transition, Water, and Technology solutions. This was largely offset by a softer UK market, where revenues declined by 8% year-on-year due to the delayed outcome of the government’s Spending Review. In addition, a pause in Australia’s infrastructure market and a shift in our US Environment business towards a higher quality portfolio also weighed on overall growth.

Total backlog was supported by significant order intake from clients in Pharmaceuticals, Data Centers, Energy Transition, US Water, and Rail, offsetting contracts winding down in US Environmental Restoration, Semiconductors and Mobility clients in UK and Australia.

We are well positioned for growth in the second half of 2025, supported by the ramp‑up of large contracts, increased UK spending, and improved market stability.

OPERATING EBITA MARGIN

Operating EBITA margin was 11.3% for the quarter, up from last year’s underlying margin of 10.8% after adjusting for the €6.6 million Middle East provision release. Margin improvement was supported by strategic levers, including the expansion of our Key Clients program, now representing 67% of Net Revenues (up from 59% last year) and a rise in Global Excellence Centers’ contribution to 15% (from 13% last year), with headcount now at 5,100 and preparations for the opening of our new center in Bucharest, Romania underway. Continued project selectivity, combined with ongoing investments in people and digital platforms, supported further efficiency gains. We remain on track with our strong margin trajectory towards the 12.5% target for 2026.

REVIEW OF THE HALF YEAR 2025

PROFIT & LOSS ITEMS

Net revenues totaled €1,937 million and were stable on an organic basis year-on-year. The operating EBITA margin was strong at 11.1% (H1‘24: 11.1%1)). Non-operating costs were €31 million, driven by right-sizing and restructuring efforts mainly in the UK in the first quarter. Net finance expenses decreased to €20 million (H1‘24: €23 million), mostly driven by on average lower interest rates on loans and borrowings. Net income from operations decreased by 4% to €121 million (H1‘24: €126 million), or €1.35 per share (H1‘24: €1.40).

BALANCE SHEET & CASH FLOW

Days Sales Outstanding (DSO) was 68 days at the end of H1’25 (H1‘24: 66 days). Net Working Capital as a percentage of annualized quarterly gross revenues was 13.4% (H1‘24: 12.7%), with a strong June revenue performance driving up the receivables position. Free cash flow in the quarter was a positive €2 million resulting in €-136 million for the half year (H1‘24: €-88 million), in line with seasonal trends and impacted by €26 million higher cash out versus last year as 2024 benefitted from lower cash taxes in the US, and we made prepayments for Q4 2025. Net debt increased to €1,039 million (H1‘24: €1,016 million) leading to a Net Debt / Operating EBITDA ratio of 1.8x (H1‘24: 1.9x), well within the strategic range of 1.5-2.5x.

1) Operating EBITA Margin for H1’24 was 10.8% when excluding a one-off provision release related to Middle East of €6.6 million

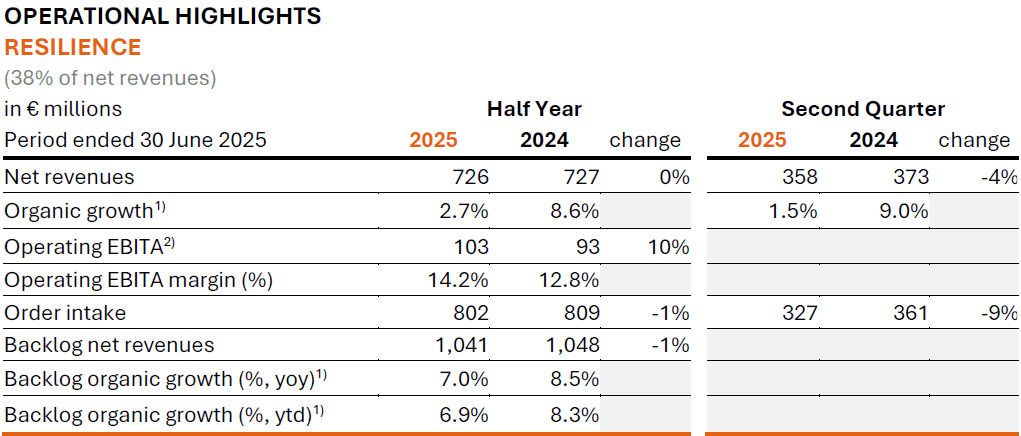

Strong growth in Energy Transition in Germany, Climate Adaptation in the Netherlands, and Water Optimization in the US was partially offset a temporary slowdown in the UK due to delays in the AMP8 cycle not offsetting reduced infrastructure-related environmental work. Strong backlog development was supported by large framework contracts renewed at the start of the year, and underpinned by key wins in Water, Energy Transition, and Nuclear. In the UK, revenue from AMP8 Water contracts is set to gradually increase, with orders starting to be called off at the end of the second quarter. Additionally, our expanding Energy Transition backlog is expected to support near-term revenue growth. The margin benefited from disciplined project selection and effective cost management. Significant investments in talent for Energy Transition and in AI-driven Water solutions further strengthens our position to capture growth opportunities in these markets.

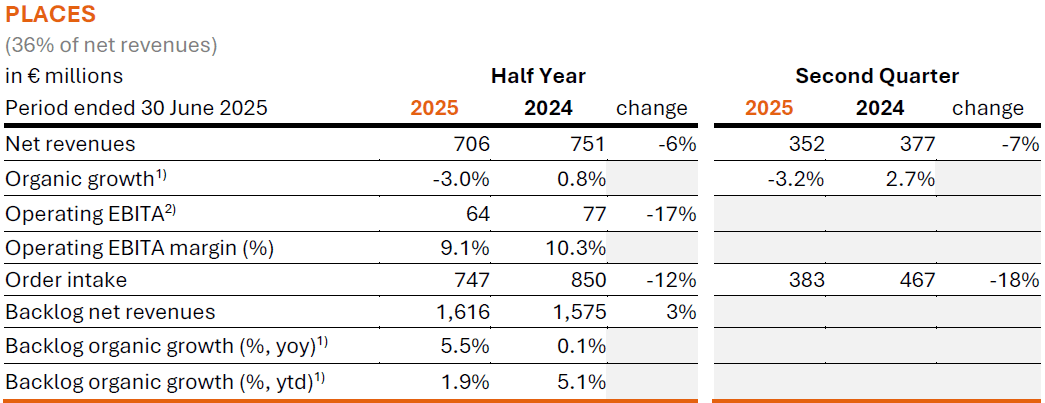

Net revenues were impacted by delays in major capital expenditure decisions from Industrial Manufacturing and Property & Investment clients, which was partially offset by strong performance in the US Pharmaceutical and Data Center sectors. The acquisition of KUA in Germany further enhanced our position in the high-growth Data Center sector. Solid order intake was supported by a significant US Pharma win, driving near term growth. Furthermore, the conclusion of the UK Spending Review and substantial European government spending plans are enhancing pipeline opportunities with Key Clients in areas such as housing, defense, transport hubs and healthcare, positioning us well for the second half of the year.

1) Underlying growth excludes the impact of FX, acquisitions, footprint reductions, winddowns or divestments

2) EBITA excludes restructuring, integration, acquisition, and divestment costs

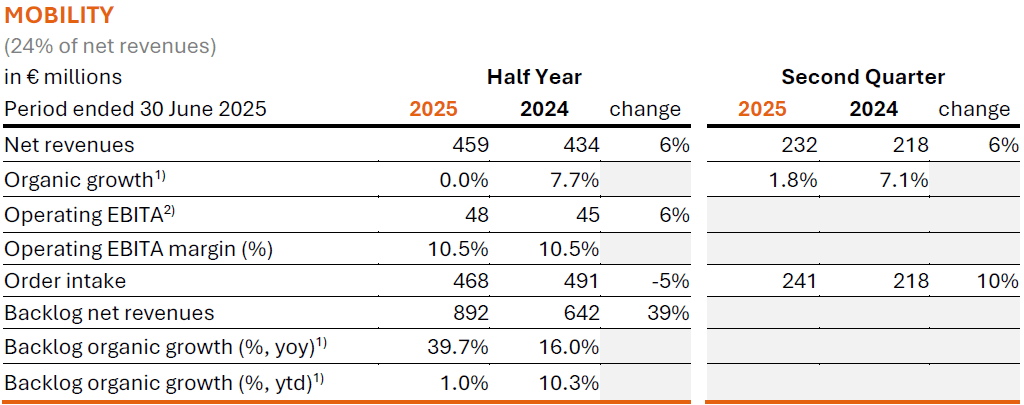

North America delivered a steady performance, supported by the planned ramp-up of large US and Canadian projects secured last

North America delivered a steady performance, supported by the planned ramp-up of large US and Canadian projects secured last