Construction is recovering rapidly from the pandemic but is exposed to material shortages.

Arcadis has tracked the issue of materials shortages and price hikes since December 2020. In this latest update, we highlight their widening impact on large construction projects.

It is important to keep price increases in context. They are the biggest material price hikes seen in 15 years, but they are affecting a narrow range of products. This Market Update summarises the key implications of recent developments and outlines mitigating actions.

Key takeaways:

- The situation regarding construction materials deteriorated in April and May, with lead-in times lengthening, prices increasing, and more materials being distributed upon allocation.

- The worst problems are currently in the domestic housing sector, where no improvement is expected before Q1 2022.

- The most exposed materials are those traded internationally, including steel and timber. Electrical products (e.g., switch gear, cable terminations and cable trays), roofing products, and PVC also present some risk.

- Currently, the infrastructure sector and buildings with a high content of materials are subject to shortages/price increases, such as industrial units, distribution centres, and data centres, are most exposed. As contractors are not always able to pass costs onto clients, there is still evidence of competitive bidding in some market sectors.

- Tier 1 and the larger Tier 2 contractors are expected to be able to secure materials required for their projects, subject to sufficient lead-in periods. Availability problems are mostly affecting small to medium-sized projects.

- Risk exposure on projects includes price inflation, extended lead-in times, and disruption caused by managing contractors’ poor supply chain management.

- Clients are advised to evaluate the exposure of their schemes and designs to the materials most at risk, and to review procurement and construction programs to allow for sufficient lead-in times.

- Proactive communication with the supply chain, regular demand forecasting, and early procurement is also recommended.

- Our assessment indicates that material supply constraints and commodity price increases will add between 2% and 4% to total project costs, depending on a project’s material content.

- We also anticipate logistics and transportation could add a further 1% to 3% to project costs. Again, this will be entirely dependent on the volume of overseas imports required to deliver a project.

What is happening and how long will it last?

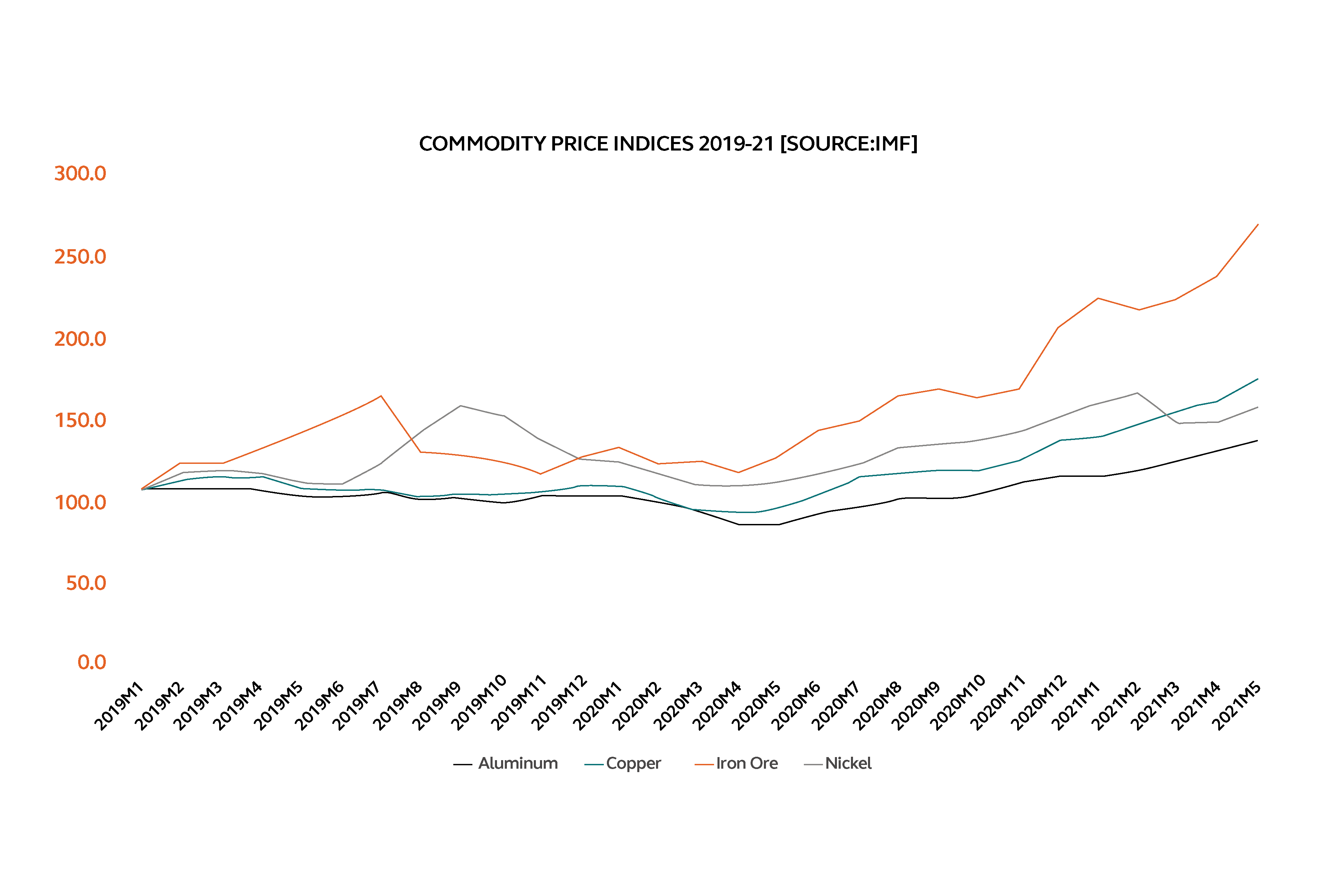

Recently reported increases in commodity prices (especially metals) are being compounded by shortages in construction materials. Previously stockpiled goods have been used, and imports are suffering from delays and increased logistics costs resulting from the COVID-19 pandemic.

In addition, during the pandemic, there was a surge in demand for building materials as Australians invested their free time and spare cash in home construction and renovation projects. This has been driven by the government’s HomeBuilder scheme. The Housing Industry Association (HIA) estimates more than 130,000 new homes will be built this year, with the scheme costing approximately $2Bn.

Australia’s ‘Black Summer’ bushfires in early 2020 created further constraints. The fires destroyed a large proportion of local hardwood and softwood, driving suppliers and contractors to alternative supply routes overseas. But sourcing timber offshore has also proven challenging. Before the pandemic, timber imports accounted for approximately 25% of Australia’s total supply. In the current climate, these imports have dropped significantly, largely due to constraints on global freight and shipping containers.

Overall, the scope of materials affected is relatively limited, with most news headlines reflecting the situation in the domestic residential sector. However, the problem now extends beyond commodity prices and logistics. Physical demand for materials exceeds the industry’s capacity to supply, with manufacturers and suppliers using allocation systems to avoid major shortages.

The forecast increase in building activity in both the infrastructure and property sectors is likely to further constrain supply capacity, at least in the short-term. The situation will worsen before it improves and we do not expect a return to “normal” before the beginning of 2022.

What does this mean for your project?

The present situation will impact most projects to some degree, depending on their work content, procurement strategy and the timing of purchases.

- Projects such as distribution centres and infrastructure projects, with high exposure to basic materials — including steel sections and rebar — and with a lack of alternative products, are likely to see costs pass quickly through the supply chain. Similarly, the volume housebuilding sector is most exposed to shortages in timber, roofing, and PVC products.

- Collaborative contracts that include some risk sharing, such as a target costs, will more likely expose clients to cost increases via a cost reimbursement mechanism. Lump sum contracts provide an element of protection, but this depends on when procurement activities are undertaken (and when contracts are signed and executed).

- Material cost increases on projects procured on a two-stage or ECI basis are more likely to be passed through to the final contract sum. Single stage tenders are more competitive but will increasingly become less acceptable to bidders.

- The reality is that global material price volatility presents contractors with cost escalation issues. Therefore, many contractors are looking to hold their tender pricing for no more than 30 days rather than the 90 days which has been the industry norm in the last few years.

- For projects with a greater value-added content, or in markets which remain competitive, some or all materials cost increases are still being absorbed by the supply chain. This may lead to difficulties, relating to the financial stability of the supply chain or negative contractual behaviours, further down the line.

Consequences will, in the first instance, arise from potential project delays due to longer lead-in times. This can be mitigated by early procurement and market engagement activities.

The overall and potential cost impact will be unique to each project as outlined above.

Extended lead-in times add further complication to projects with very tight timeframes. These projects will be more exposed to price inflation. Contractors may be forced to find alternative suppliers to those in the normal allocation systems and supply chain relationships, which may require them to pay cost premiums. This risk could be more widespread than first thought if contractors are not pro-actively managing early package procurement.

Why is this the case?

The present situation is a result of multiple factors coming into play in parallel. Throughout 2020, COVID-19 impacted both supply and demand. The latter, however, began recovering faster, driven especially by China opening its economy and its pursuit of investment across multiple construction projects. There are also wider factors at play such as the rising cost of carbon, which has added $260/tonne to the cost of rebar since the start of the year.

It is also worth noting the economic outlook across the world has been improving (with some exceptions, such as Brazil and India). Multiple governments are now pursuing construction-intensive programs to support their economic recovery, resulting in soaring demand for commodities and materials.

Australia is no exception to this.

Unfortunately, capacity has not yet returned to pre-COVID levels. Iron ore mining output is still impaired by the consequences of the dam disaster at Vale’s facility, and many manufacturers are struggling with limited availability of raw materials and capacity limitations at their own facilities.

In addition, the prices of both containers and dry bulk shipping are skyrocketing, with serious shortages in haulage between Australia and other countries. The faster than expected recovery in demand has coincided with increasing pressure on the availability of construction materials. This problem has intensified since we flagged it in our Autumn Forecast. What started in late 2020 as a combination of constrained manufacturing capacity and increasing logistics costs has escalated to significant shortages, extensions of lead times by several weeks, and spikes in the prices of steel, timber, and concrete. Logistics costs remain historically high and material prices continue increasing. Incidents like the recent blockade of the Suez Canal do not help supply constraints.

While the current issues around logistics and capacity should ease with time, there may still be some pressure resulting from demand outstripping 2019 capacity levels.

Which materials have been most impacted?

Firstly, it must be stated that, while categories of products face significant price hikes, most construction materials have remained within the anticipated ~3% annual price increase. Based upon data available to the end of March 2021, materials that have NOT been impacted comprise:

- Ready mixed concrete

- Pipes and fittings

- Cement

- Paint (both aqueous and non-aqueous)

- Ironmongery/door furniture

- Painting and decorating finishes

- Screws

Reported pressure on material availability is especially relevant to the infrastructure sector, which is anticipated to expand rapidly as on-site work increases. In particular, the cost of steel and timber is reflected in higher-than-usual increases for construction goods containing these materials.

There is presently very little information on cost inflation pressures affecting the engineering services sector. M&E is highly exposed to commodity prices associated with copper cable etc., but there is a very high value-added component in M&E materials so the inflation pass-through will not be as high as for many basic materials.

So, what is the cost impact on projects?

The cost impact will permeate to different extents on new build and refurbishment projects. However, in both categories, some items will be sensitive to increases in commodity pricing. At the time of writing, many contractors appear to be absorbing the additional costs imposed by the supply chain within their competitive pricing. However, as this situation continues to persist, it is highly doubtful that contractors will continue to absorb these cost premiums.

Our assessment indicates that, towards the end of this year at the latest, material supply constraints and commodity price increases, will add between 2% and 4% on total project costs, depending on the project’s material content. We also anticipate logistics and transportation could add between a further 1% and 3% to project costs, depending on the volume of overseas imports required to deliver the project.

What can be done to mitigate material supply and cost risks on your projects?

Research by Arcadis indicates 34% of total project delivery costs can be influenced by procurement strategy. This includes risk, contractor’s margin, and management costs. The remaining 66% of project delivery costs (comprising labour, plant, and materials) is influenced by wider market forces. With this in mind, we have provided below an indication of steps you can take to reduce project cost and risk:

- Review short and mid-term investment priorities and evaluate the potential exposure to inflation risks.

- Review the procurement strategy with respect to the competitive position of the project and your risk appetite.

- If your project is time constrained, undertake a detailed risk review and consider mitigations associated with cost and lead-in times.

- Undertake proactive communication with the supply chain to understand current limitations and the potential impact of delays and costs on the project.

- Undertake Value Management exercise and Contingency Management scenarios from the outset.

- Instigate optioneering assessments as early as possible to identify material supply issues, assess alternatives, and place advance orders where required.